Cloudflare Q2 Earnings: Buy, Sell, or Hold?

Cloudflare’s Q2 2025 Financial Outlook

Cloudflare is set to release its second-quarter 2025 financial results on July 31, 2025. The company has projected revenues between $500 million and $501 million for the quarter. This estimate aligns closely with the Zacks Consensus Estimate of $500.7 million, suggesting a year-over-year growth of 24.87%.

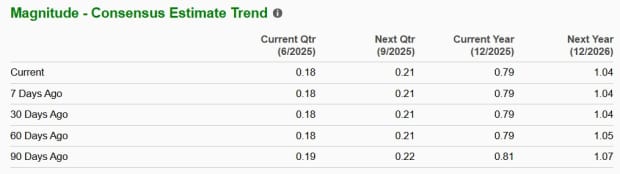

In terms of earnings, Cloudflare expects non-GAAP earnings of 18 cents per share for the second quarter. The Zacks Consensus Estimate for first-quarter earnings was also 18 cents per share, representing a 10% decline from the same period last year. Notably, the consensus estimate for earnings has remained unchanged over the past 60 days.

Earnings Performance and Market Expectations

Over the past four quarters, Cloudflare has beaten the Zacks Consensus Estimate in three instances and missed it once. On average, the earnings surprise has been 14.88%, indicating a mixed performance. However, current market expectations suggest that this quarter may not be one of the beats.

The company’s earnings forecast is influenced by several factors. Despite a positive Earnings ESP of +3.98%, Cloudflare currently holds a Zacks Rank of #5 (Strong Sell). This combination of a positive Earnings ESP and a high Zacks Rank does not typically result in an earnings beat. Investors looking to identify stocks that may exceed expectations can utilize tools like the Earnings ESP Filter.

Factors Affecting Q2 Results

Cloudflare’s Q2 results are likely to benefit from the ongoing shift in enterprise cybersecurity strategies towards zero-trust approaches. This transition has led to increased demand for Cloudflare’s services. Additionally, the company has seen a rise in high-value contracts, which have contributed to revenue growth.

Geographic expansion has also played a significant role in boosting Cloudflare’s revenues. Approximately 50% of its 2024 revenues came from outside the United States, and this percentage rose to 51% in the first quarter of 2025. The company’s diverse customer base has further supported its top-line growth, with the addition of around 13,105 new paying customers in the first quarter, bringing the total to approximately 250,819.

Cloudflare also added 30 new large customers with annual billings exceeding $100,000, increasing the total to 3,527 at the end of the first quarter. This trend of expanding the customer base has persisted for the past 15 quarters and is expected to continue in the upcoming quarter.

Challenges and Competitive Landscape

Despite these positives, Cloudflare faces challenges due to geopolitical and macroeconomic conditions. These factors have made it difficult to close large deals, impacting revenue recognition. Customer caution in IT spending and vendor onboarding, driven by recent policy changes, has negatively affected the company’s top-line growth.

Cloudflare’s stock has performed well, surging 84.2% year-to-date, outperforming the Zacks Internet – Software industry’s growth of 17.4%. However, the stock is currently trading at a premium, with a forward 12-month P/S ratio of 28.58X compared to the industry average of 5.82X. This stretched valuation raises concerns about its long-term prospects.

Investment Considerations

Cloudflare is experiencing growth through funding deals where customers commit large sums for flexible usage. These contracts can delay revenue recognition, affecting metrics like Dollar-Based Net Retention, which remained flat at 111% in the first quarter of 2025.

The competitive landscape is intense, with established players like Akamai Technologies, Amazon Web Services, and Palo Alto Networks posing significant threats. These companies offer similar services and are actively expanding their market presence. New entrants and niche players further add to the competitive pressure.

To remain competitive, Cloudflare has invested heavily in sales and marketing, particularly in international markets. These investments have impacted operating margins, with bottom-line growth projected at mid-single digits for full-year 2025.

Conclusion: A Cautionary Note

While Cloudflare’s growth prospects are strong, its current overvaluation, delayed revenue recognition, and shrinking margins make it a risky investment. Given these factors, investors may want to consider avoiding Cloudflare stock at this time.

Which one are you watching, Xplorianz? Drop your take on the most underrated pick this week in the comments!. Slide into our inbox Facebook, or tag us on X . Stay sharp, stay weird, and keep Xploring

Disclaimer:

236 XplorFiThis article is for informational and entertainment purposes only and does not constitute financial advice. Always do your own research (DYOR) before making any investment decisions, your money, your call. Crypto’s wild, so stay sharp out there!

V.F. Corp Prepares for Q1 Earnings Amid Vans Restructuring Challenges

What’s Next for Roku Stock After Q2 Earnings?

Will Amazon Stock Rise After Q2 Earnings?

Tidak ada komentar