Will Amazon Stock Rise After Q2 Earnings?

Amazon’s Q2 2025 Earnings Outlook and Strategic Developments

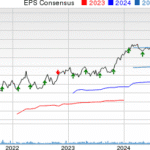

Amazon (AMZN) is set to release its second-quarter 2025 results on July 31, with expectations for net sales ranging between $159 billion and $164 billion. This projection reflects a growth rate of 7-11% compared to the same period in 2024, factoring in an estimated 10 basis points negative impact from foreign exchange fluctuations.

The Zacks Consensus Estimate for net sales stands at $162.28 billion, suggesting a 9.67% increase from the previous year. For earnings, the estimate is $1.33 per share, signaling an 8.13% growth over the prior-year quarter. These figures highlight the company’s strong performance and market confidence.

Strong Earnings Performance and Surprises

Amazon has consistently exceeded expectations in recent quarters. In the last reported quarter, the company delivered an earnings surprise of 17.78%, with each of the past four quarters beating the Zacks Consensus Estimate. The average earnings surprise over this period was 20.68%, underscoring the company’s ability to outperform financial forecasts.

The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy) or #2 (Buy) increases the likelihood of another earnings beat. Currently, AMZN has an Earnings ESP of +7.37% and holds a Zacks Rank #1, indicating strong investor sentiment.

Key Factors Influencing Q2 Results

Amazon entered the second quarter with momentum from its first-quarter results, which saw $155.7 billion in net sales. The company demonstrated resilience in navigating macroeconomic challenges while maintaining growth.

AWS and AI Initiatives

Amazon Web Services (AWS) remains a key driver of growth, with model estimates projecting 16.9% year-over-year revenue growth to $30.72 billion in the upcoming quarter. The launch of Amazon Nova models gained traction during the quarter, including the Nova Sonic speech-to-speech foundation model and Nova Act SDK, which enable developers to build advanced voice-based AI applications.

The rollout of Trainium 2 chips further strengthened AWS’ competitive position, offering customers 30-40% better price performance than GPU-based instances. This advancement positions AWS to capture increased demand in the AI infrastructure market.

Advertising, E-commerce, and Physical Retail Growth

Amazon’s advertising segment showed robust growth, with first-quarter revenues reaching $13.9 billion, up 19% year-over-year. The platform’s reach extended to over 275 million users in the U.S., providing significant scale for brand partners.

E-commerce benefits from improved fulfillment network efficiency, with model estimates predicting $60.2 billion in online store revenues, a 8.8% increase from the previous year. The focus on everyday essentials drove growth, with this category representing one-third of units sold in the U.S.

Physical retail operations are also expected to grow, with model estimates projecting $5.38 billion in sales, a 3.4% increase from the prior year. The integration of technologies like Amazon Dash Cart enhances the omnichannel experience.

Third-party seller services remain a major growth driver, with model estimates pegged at $39.1 billion, reflecting an 8.3% year-over-year increase.

Prime Day and Enhanced Customer Experience

Amazon’s redesigned inbound network architecture improved inventory placement and delivery speeds, enhancing the customer experience during high-volume periods. Record delivery speeds for Prime members set a strong foundation for the current quarter.

The introduction of Alexa+ gained traction, with over 100,000 users during its initial rollout. This next-generation personal assistant represents a significant advancement in smart home technology.

International Expansion and Innovation

Amazon’s international operations showed resilience, with 8% growth excluding foreign exchange impacts in the first quarter. The launch of Amazon.ie in Ireland expanded the company’s European footprint. Luxury shopping through Saks on Amazon and partnerships with brands like Michael Kors and The Ordinary diversified product offerings.

Project Kuiper reached a significant milestone with successful satellite launches, positioning Amazon to begin customer service in 2025. The company’s investment in logistics infrastructure, including a $4 billion commitment to expand rural delivery networks, strengthens its competitive advantages.

Stock Valuation and Investment Thesis

Shares of Amazon have gained 5.5% year-to-date, slightly underperforming the broader Zacks Retail-Wholesale sector and the S&P 500 index. However, AMZN trades at a premium, with a forward 12-month P/S ratio of 3.34X compared to the industry average of 2.17X.

Despite the stretched valuation, Amazon’s diversified ecosystem, including high-growth AWS cloud services, robust advertising momentum, and optimized e-commerce operations, creates multiple revenue catalysts. Strategic investments in AI infrastructure, international expansion, and emerging technologies like Project Kuiper establish sustainable competitive moats.

Conclusion

Amazon’s integrated platform spanning cloud, retail, and emerging technologies positions it as a compelling buy for long-term investors. While facing intense competition, the company’s growth trajectory and strategic initiatives justify current valuations. With strong earnings potential and a focus on innovation, Amazon remains a key player in the tech and retail landscape.

Which one are you watching, Xplorianz? Drop your take on the most underrated pick this week in the comments!. Slide into our inbox Facebook, or tag us on X . Stay sharp, stay weird, and keep Xploring

Disclaimer:

106 XplorFiThis article is for informational and entertainment purposes only and does not constitute financial advice. Always do your own research (DYOR) before making any investment decisions, your money, your call. Crypto’s wild, so stay sharp out there!

Blue Ridge Bankshares Plummets Despite Q2 Profit Return

Microsoft Stock Fans, Mark Your Calendars for August 1

V.F. Corp Prepares for Q1 Earnings Amid Vans Restructuring Challenges

What’s Next for Roku Stock After Q2 Earnings?

Tidak ada komentar